Introduction to Inventory

and Cost of Goods Sold

Inventory is merchandise purchased by merchandisers (retailers,

wholesalers, distributors) for the purpose of being sold to customers. The cost

of the merchandise purchased but not yet sold is reported in the account

Inventory or Merchandise Inventory.

Inventory is reported as a current asset on the company's balance sheet. Inventory is a significant asset

that needs to be monitored closely. Too much inventory

can result in cash flow problems, additional expenses (e.g., storage,

insurance), and losses if the items become obsolete. Too little inventory

can result in lost sales and lost customers.

Because of the cost principle, inventory is reported on the balance sheet at the amount

paid to obtain (purchase) the merchandise, not at its selling price.

Inventory is also a significant asset of manufacturers. However,

in order to simplify our explanation, we will focus on a retailer.

Cost of Goods Sold

Cost of goods sold is the cost of the

merchandise that was sold to customers. The cost of goods

sold is reported on the income statement when the

sales revenues of the goods sold are reported.

A retailer's cost of goods sold

includes the cost from its supplier plus any

additional costs necessary to get the merchandise into inventory and ready for

sale. For example, let's assume that Corner Shelf Bookstore purchases a college

textbook from a publisher. If Corner Shelf's cost from the publisher is $80 for

the textbook plus $5 in shipping costs, Corner Shelf reports $85 in its

Inventory account until the book is sold. When the book is sold, the $85 is

removed from inventory and is reported as cost of goods sold on the income

statement.

When Costs Change

If the publisher increases the

selling prices of its books, the bookstore will have a higher cost for

the next book it purchases from the publisher. Any books in the

bookstore's inventory will continue to be reported at their cost when

purchased. For example, if the Corner Shelf Bookstore has on its shelf a book

that had a cost of $85, Corner Shelf will continue to report the cost of that

one book at its actual cost of $85 even if the same book now has a cost of $90.

The cost principle will not allow an amount higher than cost to be included in

inventory.

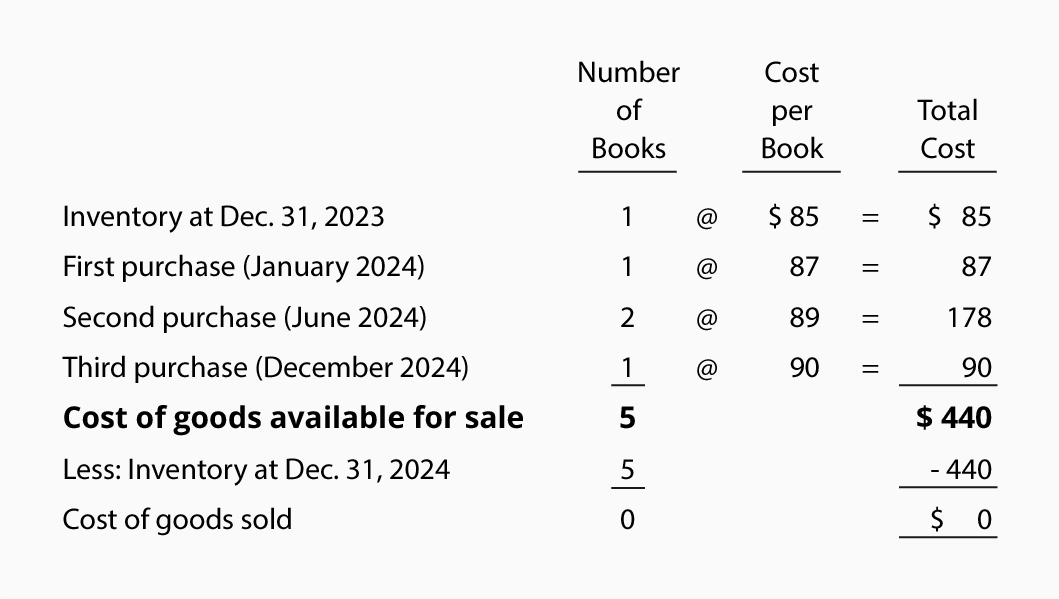

Let's assume the Corner Shelf Bookstore had one book in

inventory at the start of the year 2014 and at different times during 2014

purchased four identical books. During the year 2014 the cost of these books

increased due to a paper shortage. The following chart shows the costs of the

five books that have to be accounted for. It also assumes that none of the

books has been sold as of December 31, 2014.

Special Feature: Review what you are

learning by working the three interactive crossword puzzles dedicated to this

topic. They are completely free. Inventory & Cost of Goods Sold Puzzles

Cost Flow Assumptions

If the Corner Shelf Bookstore sells only one of the five books,

which cost should Corner Shelf report as the cost of goods sold? Should it

select $85, $87, $89, $89, $90, or an average of the five amounts? A related

question is which cost should Corner Shelf report as inventory on its balance

sheet for the four books that have not been sold?

Accounting rules allow the

bookstore to move the cost from inventory to the cost of goods sold by using

one of three cost flows:

- First

In, First Out (FIFO)

- Last

In, First Out (LIFO)

- Average

Note that these are cost flow

assumptions. This means that the order in which costs are

removed from inventory can be different from the order in which the goods are

physically removed from inventory. In other words, Corner Shelf could sell the

book that was on hand at December 31, 2013 but could remove from inventory the

$90 costof the book purchased in December 2014 (if it elects the LIFO

cost flow assumption).

Inventory Systems

Each of the three cost flow assumptions listed above

can be used in either of two systems (or methods) of inventory:

A. Periodic

B. Perpetual

B. Perpetual

A. Periodic inventory system. Under this system the amount

appearing in the Inventory account is not updated when purchases of merchandise

are made from suppliers. Rather, the Inventory account is commonly updated or

adjusted only once—at the end of the year. During the year the Inventory

account will likely show only the cost of inventory at the end of the previous

year.

Under the periodic inventory

system, purchases of merchandise are recorded in one or more Purchasesaccounts.

At the end of the year the Purchases account(s) are closed and the Inventory

account is adjusted to equal the cost of the merchandise actually on hand at

the end of the year. Under the periodic system there is noCost of Goods Sold account

to be updated when a sale of merchandise occurs.

In short, under the periodic inventory system there is

no way to tell from the general ledger accounts the amount of inventory or the

cost of goods sold.

B. Perpetual inventory system. Under this system the

Inventory account is continuously updated. The Inventory account is increased

with the cost of merchandise purchased from suppliers and it is reduced by the

cost of merchandise that has been sold to customers. (The Purchases account(s)

do not exist.)

Under the perpetual system there is a Cost of Goods

Sold account that is debited at the time of each sale for the cost of the

merchandise that was sold. Under the perpetual system a sale of merchandise

will result in two journal entries: one to record the sale and the cash or

accounts receivable, and one to reduce inventory and to increase cost of goods

sold.

Inventory Systems and Cost Flows

Combined

The combination of the three cost flow assumptions and

the two inventory systems results in six available options when accounting for

the cost of inventory and calculating the cost of goods sold:

A1. Periodic FIFO

A2. Periodic LIFO

A3. Periodic Average

B1. Perpetual FIFO

B2. Perpetual LIFO

B3. Perpetual Average

A2. Periodic LIFO

A3. Periodic Average

B1. Perpetual FIFO

B2. Perpetual LIFO

B3. Perpetual Average

A1. Periodic FIFO

"Periodic" means that the Inventory account

is not routinely updated during the accounting period. Instead, the cost of

merchandise purchased from suppliers is debited to an account called Purchases.

At the end of the accounting year the Inventory account is adjusted to equal

the cost of the merchandise that has not been sold. The cost of goods sold that

will be reported on the income statement will be computed by taking the cost of

the goods purchased and subtracting the increase in inventory (or adding the

decrease in inventory).

"FIFO"

is an acronym for First In, First Out. Under the FIFO cost flow assumption, the first

(oldest) costs are the first ones to leave inventory and become the cost of

goods sold on the income statement. The last (or recent) costs will be reported

as inventory on the balance sheet.

Remember that the costs can flow differently than the

goods. If the Corner Shelf Bookstore uses FIFO, the owner may sell the newest

book to a customer, but is allowed to report the cost of goods sold as $85 (the

first, oldest cost).

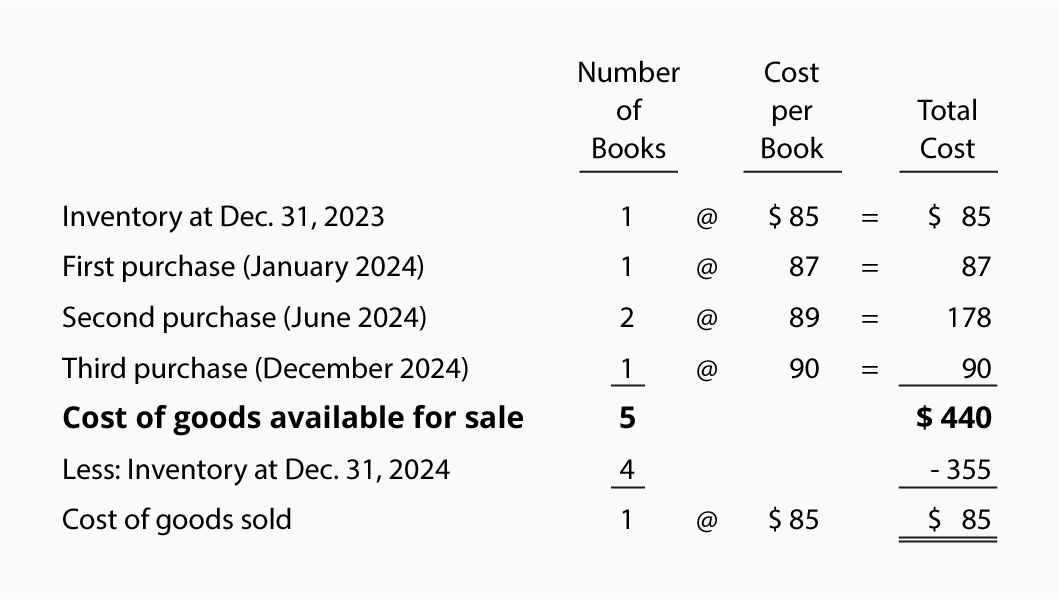

Let's illustrate periodic FIFO with the amounts from

the Corner Shelf Bookstore:

As before, we need to account for the total goods

available for sale (5 books at a cost of $440). Under FIFO we assign the first

cost of $85 to the one book that was sold. The remaining $355 ($440 - $85) is

assigned to inventory. The $355 of inventory costs consists of $87 + $89 + $89

+ $90. The $85 cost assigned to the book sold is permanently gone from

inventory.

If Corner Shelf Bookstore sells

the textbook for $110, its gross profit under periodic

FIFO will be $25 ($110 - $85). If the costs of textbooks continue to increase,

FIFO will always result in more profit than other cost flows, because the first

cost is always lower.

A2. Periodic LIFO

"Periodic" means that

the Inventory account is not updated during the accounting period.

Instead, the cost of merchandise purchased from suppliers is debited to an

account called Purchases. At the end of the accounting year the Inventory

account is adjusted to equal the cost of the merchandise that is unsold. The

other costs of goods will be reported on the income statement as the cost of

goods sold.

"LIFO" is an acronym for Last In, First Out. Under the LIFO cost flow

assumption, the last (or recent) costs are the first ones to leave inventory

and become the cost of goods sold on the income statement. The first (or

oldest) costs will be reported as inventory on the balance sheet.

Remember that the costs can flow differently than the

goods. In other words, if Corner Shelf Bookstore uses LIFO, the owner may sell

the oldest (first) book to a customer, but can report the cost of goods sold of

$90 (the last cost).

It's important to note that under LIFO

periodic (not

LIFO perpetual) we wait until the entire year is over before assigning the

costs. Then we flow the year's last costs first, even if those goods arrived after the last sale of the year. For example, assume the

last sale of the year at the Corner Shelf Bookstore occurred on December 27.

Also assume that the store's last purchase of the year arrived on December 31.

Under LIFO periodic, the cost of the book purchased on December 31 is sent to

the cost of goods sold first, even though it's physically

impossible for that book to be the one sold on December 27. (This reinforces

our previous statement that the flow of costs does not have to correspond with

the physical flow of units.)

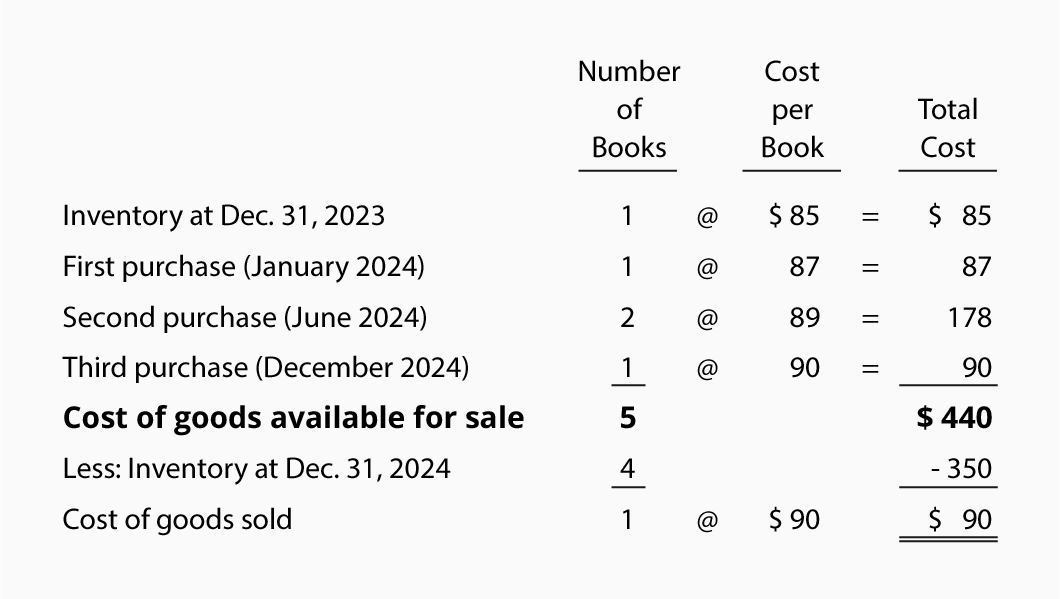

Let's illustrate periodic LIFO by using the data for

the Corner Shelf Bookstore:

As before we need to account for the total goods

available for sale: 5 books at a cost of $440. Under periodic LIFO we assign

the last cost of $90 to the one book that was sold. (If two books were sold,

$90 would be assigned to the first book and $89 to the second book.) The

remaining $350 ($440 - $90) is assigned to inventory. The $350 of inventory

cost consists of $85 + $87 + $89 + $89. The $90 assigned to the book that was

sold is permanently gone from inventory.

If the bookstore sold the

textbook for $110, its gross profit under

periodic LIFO will be $20 ($110 - $90). If the costs of textbooks continue to

increase, LIFO will always result in the least amount of profit. (The reason is

that the last costs will always be higher than the first costs. Higher costs

result in less profits and usually lower income taxes.)

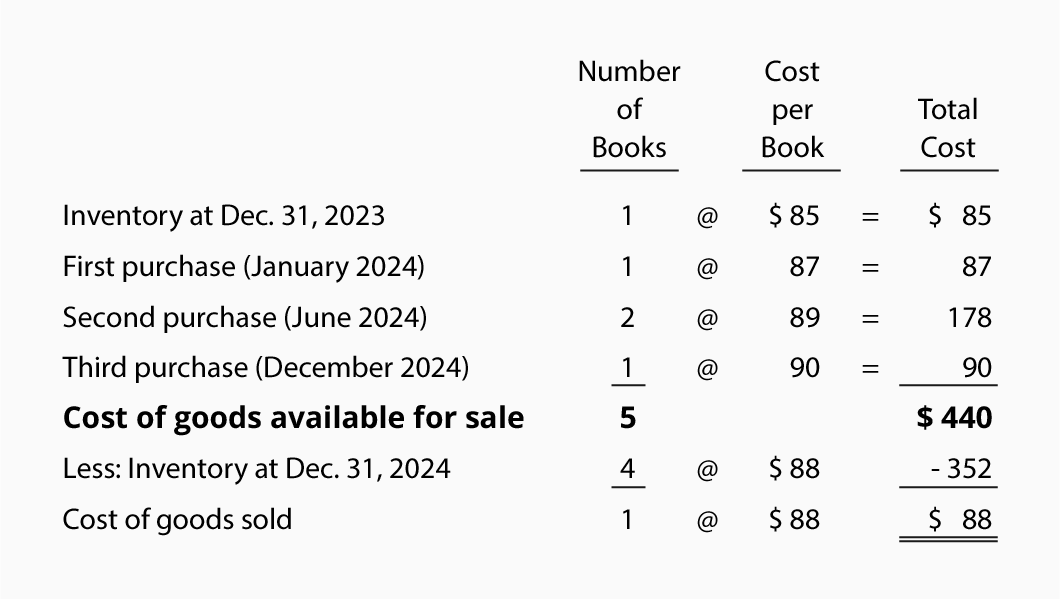

A3. Periodic Average

Under "periodic" the

Inventory account is not updated and purchases of merchandise are recorded in

an account called Purchases. Under this cost flow assumption an average cost is

calculated using the total goods available for sale (cost from the beginning

inventory plus the costs of all subsequent

purchases made during the entire year). In other words, the periodic average

cost is calculated after the year is over—after all the purchases of the year

have occurred. This average cost is then applied to the units sold during the

year as well as to the units in inventory at the end of the year.

As you can see, our facts remain

the same-there are 5 books available for sale for the year 2014 and the cost of

the goods available is $440. The weighted

average cost of

the books is $88 ($440

of cost of goods available ÷ 5 books available) and it is used for both the

cost of goods sold and for the cost of the books in inventory.

Since the bookstore sold only one

book, the cost of goods sold is $88 (1

x $88). The four books still on hand are reported at $352 (4 x $88) of cost in the Inventory account. The total

of the cost of goods sold plus the cost of the inventory should equal the total

cost of goods available ($88 + $352 = $440).

If Corner Shelf Bookstore sells the textbook for $110,

its gross profit under the periodic average method will be $22 ($110 - $88).

This gross profit is between the $25 computed under periodic FIFO and the $20

computed under periodic LIFO.

Perpetual FIFO

Under the perpetual system the Inventory account is constantly (or perpetually) changing. When

a retailer purchases merchandise, the retailer debits its Inventory account for

the cost; when the retailer sells the merchandise to its customers its

Inventory account is credited and its Cost of Goods Sold account

is debited for the cost of the goods sold. Rather than staying dormant as it does with the periodic method, the Inventory

account balance is continuously updated.

Under the perpetual system, two

transactions are recorded when merchandise is sold: (1) the sales amount is

debited to Accounts Receivable or Cash and is credited to Sales, and (2) the cost of the merchandise sold is debited to

Cost of Goods Sold and is credited to Inventory. (Note: Under the periodic

system the second entry is not made.)

With perpetual FIFO, the first (or oldest) costs are

the first moved from the Inventory account and debited to the Cost of Goods

Sold account. The end result under perpetual FIFO is the same as under periodic

FIFO. In other words, the first costs are the same whether you move the cost

out of inventory with each sale (perpetual) or whether you wait until the year

is over (periodic).

B2. Perpetual LIFO

Under the perpetual system the

Inventory account is constantly (or perpetually) changing. When a retailer

purchases merchandise, the retailer debits its Inventory account for the cost

of the merchandise. When the retailer sells the merchandise to its customers,

the retailer credits its Inventory account for the cost of the goods that were

sold and debits its Cost of Goods Sold account for their cost. Rather than

staying dormant as

it does with the periodic method, the Inventory account balance is continuously

updated.

Under the perpetual system, two transactions are

recorded at the time that the merchandise is sold: (1) the sales amount is

debited to Accounts Receivable or Cash and is credited to Sales, and (2) the

cost of the merchandise sold is debited to Cost of Goods Sold and is credited

to Inventory. (Note: Under the periodic system the second entry is not made.)

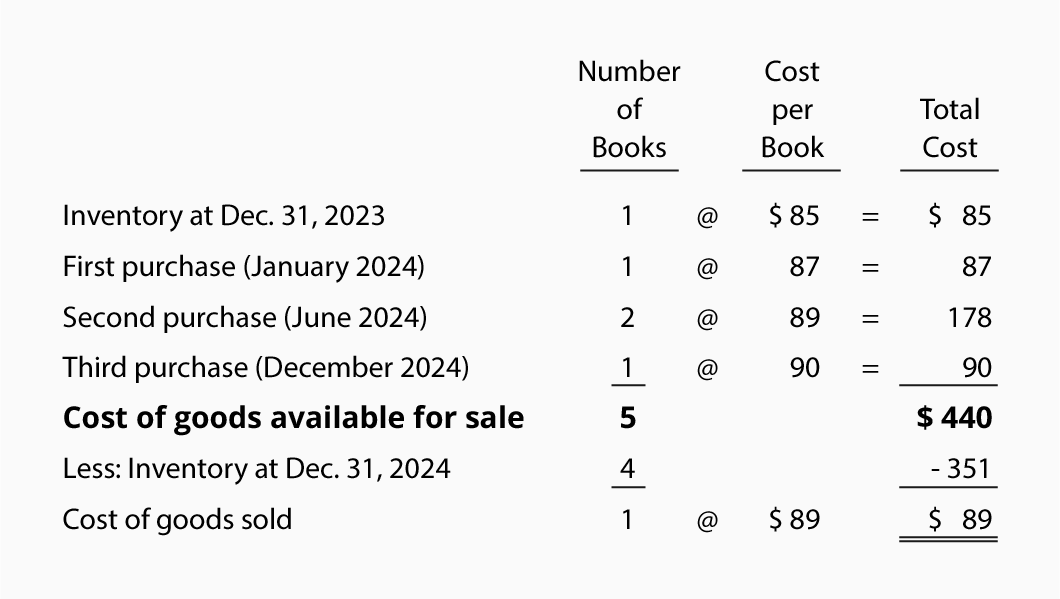

With perpetual LIFO, the last

costs available at the time of the sale are the first to be removed from the Inventory account

and debited to the Cost of Goods Sold account. Since this is the perpetual system we cannot wait until the end of the year to

determine the last cost—an entry must be recorded at

the time of the sale in

order to reduce the Inventory account and to increase the Cost of Goods Sold

account.

If costs continue to rise

throughout the entire year, perpetual LIFO

will yield a lower cost of goods sold and a higher net income than periodic LIFO. Generally this means that periodic LIFO will result in less income taxes than perpetual LIFO. (If you wish to minimize the amount paid in

income taxes during periods of inflation, you should discuss LIFO with your tax

adviser.)

Once again we'll use our example for the Corner Shelf

Bookstore:

Let's assume that after Corner Shelf makes its second purchase in June 2014,

Corner Shelf sells one book. This means the last cost at the

time of the sale was

$89. Under perpetual LIFO the following entry must be made at the time of the

sale: $89 will be credited to Inventory and $89 will be debited to Cost of

Goods Sold. If that was the only book sold during the year, at the end of the

year the Cost of Goods Sold account will have a balance of $89 and the cost in

the Inventory account will be $351 ($85

+ $87 + $89 + $90).

If the bookstore sells the textbook

for $110, its gross profit under

perpetual LIFO will be $21 ($110 - $89). Note that this is different than the

gross profit of $20 under periodic LIFO.

B3. Perpetual Average

Under the perpetual system the

Inventory account is constantly (or perpetually) changing. When a retailer

purchases merchandise, the costs are debited to its Inventory account; when the

retailer sells the merchandise to its customers the Inventory account is credited

and the Cost of Goods Sold account is debited for the cost of the goods sold.

Rather than staying dormant as

it does with the periodic method, the Inventory account balance under the

perpetual average is changing whenever a purchase or sale occurs.

Under the perpetual system, two sets of entries are

made whenever merchandise is sold: (1) the sales amount is debited to Accounts

Receivable or Cash and is credited to Sales, and (2) the cost of the

merchandise sold is debited to Cost of Goods Sold and is credited to Inventory.

(Note: Under the periodic system the second entry is not made.)

Under the perpetual system,

"average" means the average cost

of the items in inventory as of the date of the sale.

This average cost is multiplied by the number of units sold and is removed from

the Inventory account and debited to the Cost of Goods Sold account. We use the

average as of the time of the sale because this is aperpetual method. (Note: Under the periodic system we wait until the year is over before computing

the average cost.)

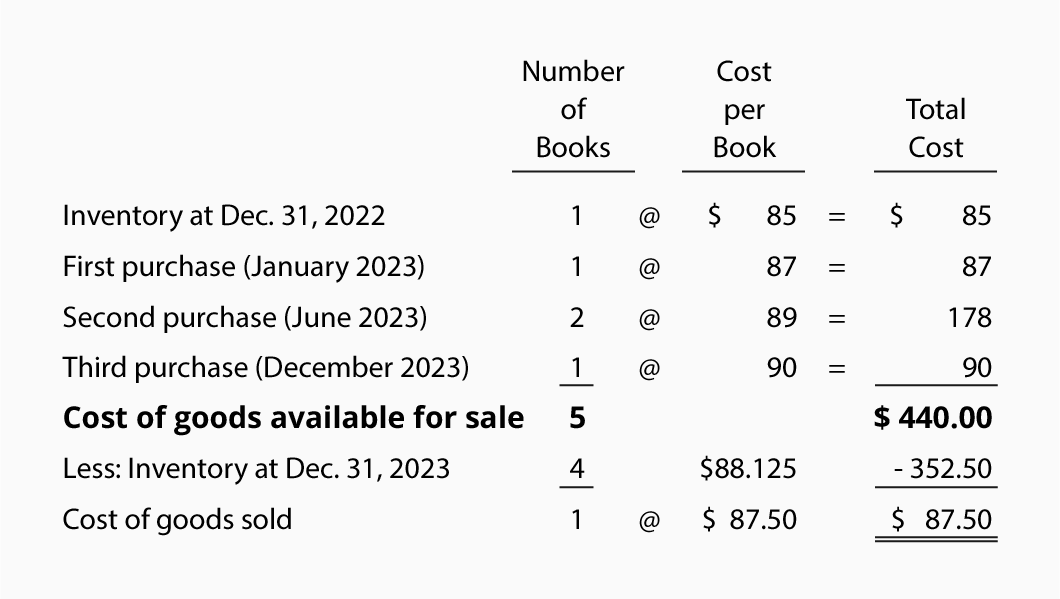

Let's use the same example again for the Corner Shelf

Bookstore:

Let's assume that after Corner

Shelf makes its second purchase, Corner Shelf sells one book. This means the

average cost at the time of the sale was $87.50 ([$85

+ $87 + $89 + $89] ÷ 4]). Because this is a perpetual average, a journal entry

must be made at the time of the sale for $87.50. The $87.50 (the average cost

at the time of the sale) is credited to Inventory and is debited to Cost of

Goods Sold. After the sale of one unit, three units remain in inventory and the

balance in the Inventory account will be $262.50 (3 books at an average cost of

$87.50).

After Corner Shelf makes its

third purchase, the average cost per unit will change to $88.125 ([$262.50 + $90] ÷ 4). As you can see, the average

cost moved from $87.50 to $88.125—this is why the perpetual average method is

sometimes referred to as the moving average method.

The Inventory balance is $352.50 (4

books with an average cost of $88.125 each).

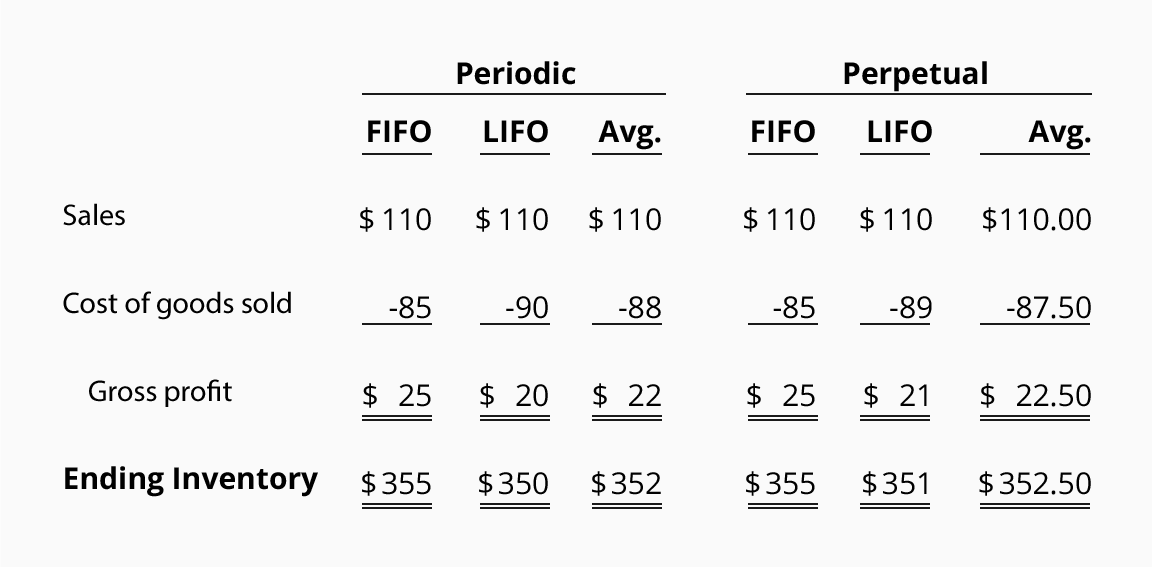

Comparison of Cost Flow Assumptions

Below is a recap of the varying amounts for the cost

of goods sold, gross profit, and ending inventory that were calculated above.

The example assumes that costs were continually

increasing. The results would be different if costs were decreasing or

increasing at a slower rate. Consult with your tax advisor concerning the

election of cost flow assumption.

Specific Identification

In addition to the six cost flow

assumptions presented in Parts 1 - 4, businesses have another option: expense

to the cost of goods sold the specific cost

of the specific item

sold. For example, Gold Dealer, Inc. has an inventory of gold and each nugget

has an identification number and the cost of the nugget. When Gold Dealer sells

a nugget, it can expense to the cost of goods sold the exact cost of the

specific nugget sold. The cost of the other nuggets will remain in inventory.

(Alternatively, Gold Dealer could use one of the other six cost flow

assumptions described in Parts 1 - 4.)

LIFO Benefits Without Tracking Units

In Part 1 and Part 2 you saw that during the periods

of increasing costs, LIFO will result in less profits. In the U.S. this can

mean less income taxes paid by the company. Most companies view lower taxes as

a significant benefit. However, the process of tracking costs and then

assigning those costs to the units sold and the units on hand could be too

expensive for the amount of income tax savings. To gain the benefit of LIFO

without the tracking of costs, there is a method known as dollar value LIFO.

This topic is discussed in intermediate accounting textbooks. The Internal

Revenue Service also allows companies to use dollar value LIFO by applying

price indexes. (You should seek the advice of an accounting and/or tax

professional to assess the cost and benefit of these techniques.)

Inventory Management

Over the past few decades sophisticated companies have

made great strides in reducing their levels of inventory. Rather than carry

large inventories, they ask their suppliers to deliver goods "just in time."

Suppliers and merchandisers have learned to coordinate their purchases and

sales so that orders and shipments occur automatically.

A company will realize significant benefits if it can

keep its inventory levels down without losing sales or production (if the

company is a manufacturer). For example, Dell Computers has greatly reduced its

inventory in relationship to its sales. Since computer components have been

dropping in costs as new technologies emerge, it benefits Dell to keep only a

very small inventory of components on hand. It would be a financial hardship if

Dell had a large quantity of parts that became obsolete or decreased in value.

Financial Ratios

Keeping track of inventory is

important. There are two common financial ratios for monitoring inventory

levels: (1) the Inventory Turnover Ratio, and (2) the Days' Sales in Inventory.

(These are discussed and illustrated in the Explanation of Financial Ratios.)

Estimating Ending Inventory

It is very time-consuming for a

company to physically count

the merchandise units in its inventory. In fact, it is not unusual for

companies to shut down their operations near the end of their accounting year

just to perform inventory counts. The company may assign one set of employees

to count and tag the items and another set to verify the counts. If a company

has outside auditors, they will be there to observe the process. (Even if the

company's computers keep track of inventory, accountants require that the

computer records be verified by actually counting the goods.)

If a company counts its inventory

only once per year it must estimate its

inventory at the end of each month in order to prepare meaningful monthly

financial statements. In fact, a company may need to estimate its inventory for

other reasons as well. For example, if a company suffers a loss due to a

disaster such as a tornado or a fire, it will need to file a claim for the

approximate cost of the inventory that was lost. (An insurance adjuster will

also compute this amount independently so that the company is not paid too much

or too little for its loss.)

Methods of Estimating Inventory

There are two methods for estimating ending inventory:

1. Gross Profit Method

2. Retail Method

2. Retail Method

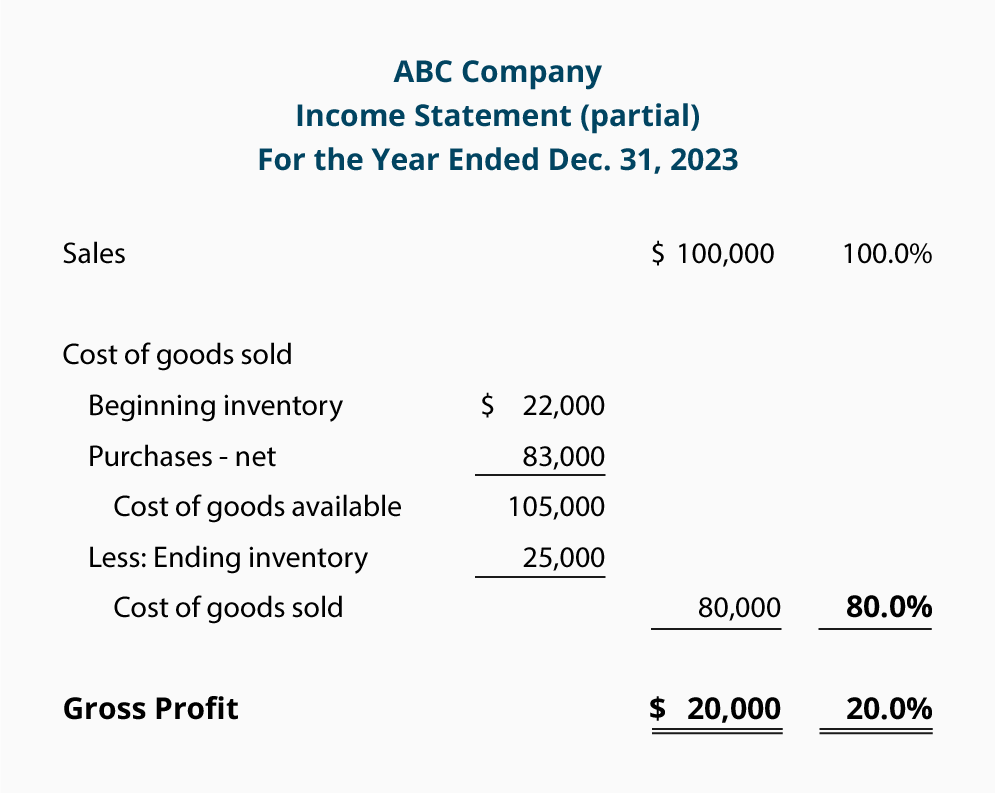

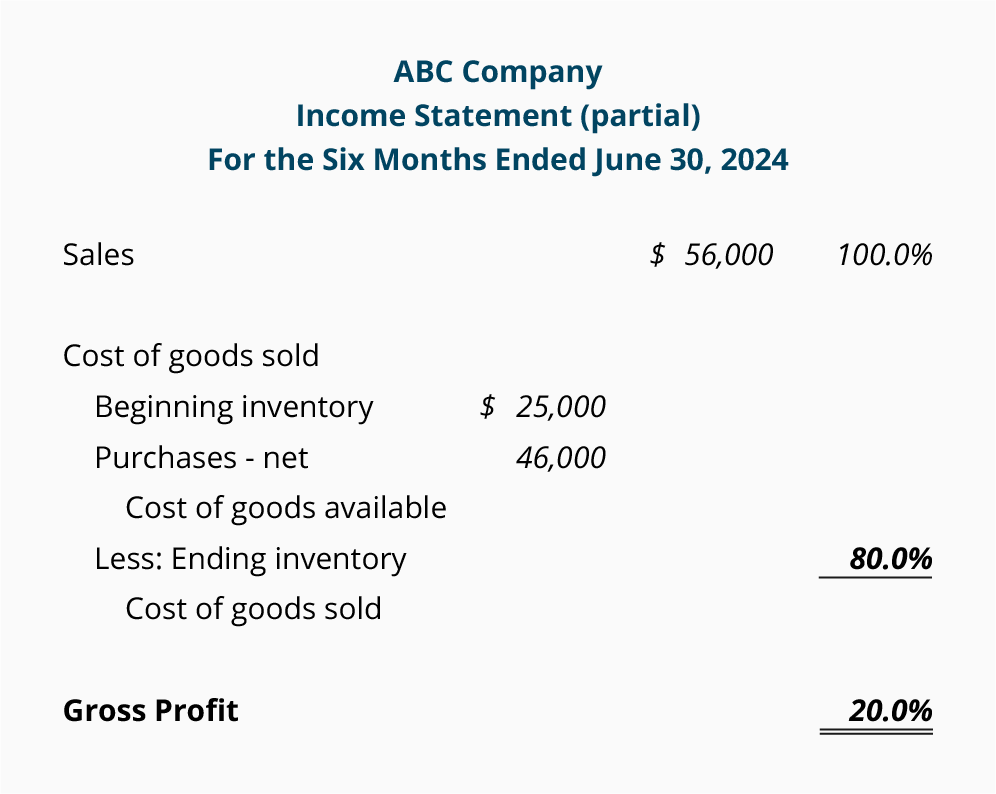

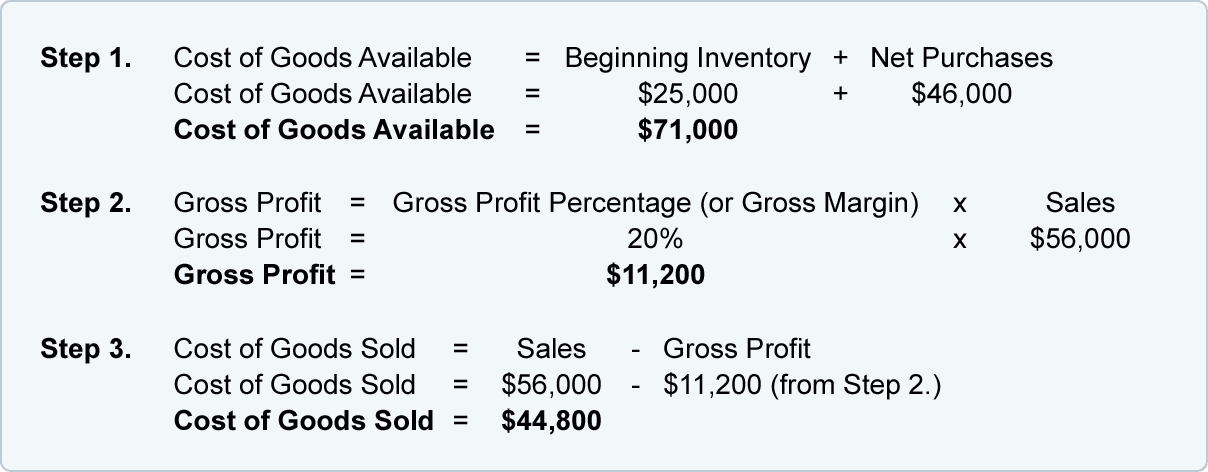

1. Gross Profit Method.

The gross profit method for estimating inventory uses the information contained

in the top portion of a merchandiser's multiple-step income statement:

Let's assume that we need to estimate the cost of inventory on hand on June 30, 2014. From

the 2013 income statement shown above we can see that the company's gross

profit is 20% of the sales and that the cost of goods sold is 80% of the sales.

If those percentages are reasonable for the current year, we can use those

percentages to help us estimate the cost of the inventory on hand as of June

30, 2014.

While an algebraic equation could be constructed to

determine the estimated amount of ending inventory, we prefer to simply use the

income statement format. We prepare a partial income statement for the period

beginning after the date when inventory was last physically counted, and ending

with the date for which we need the estimated inventory cost. In this case, the

income statement will go from January 1, 2014 until June 30, 2014.

Some of the numbers that we need are easily obtained

from sales records, customers, suppliers, earlier financial statements, etc.

For example, sales for the first half of the year 2014 are taken from the

company's records. The beginning inventory amount is the ending inventory

reported on the December 31, 2013 balance sheet. The purchases information for

the first half of 2014 is available from the company's records or its

suppliers. The amounts that we have available are written in italics in the

following partial income statement:

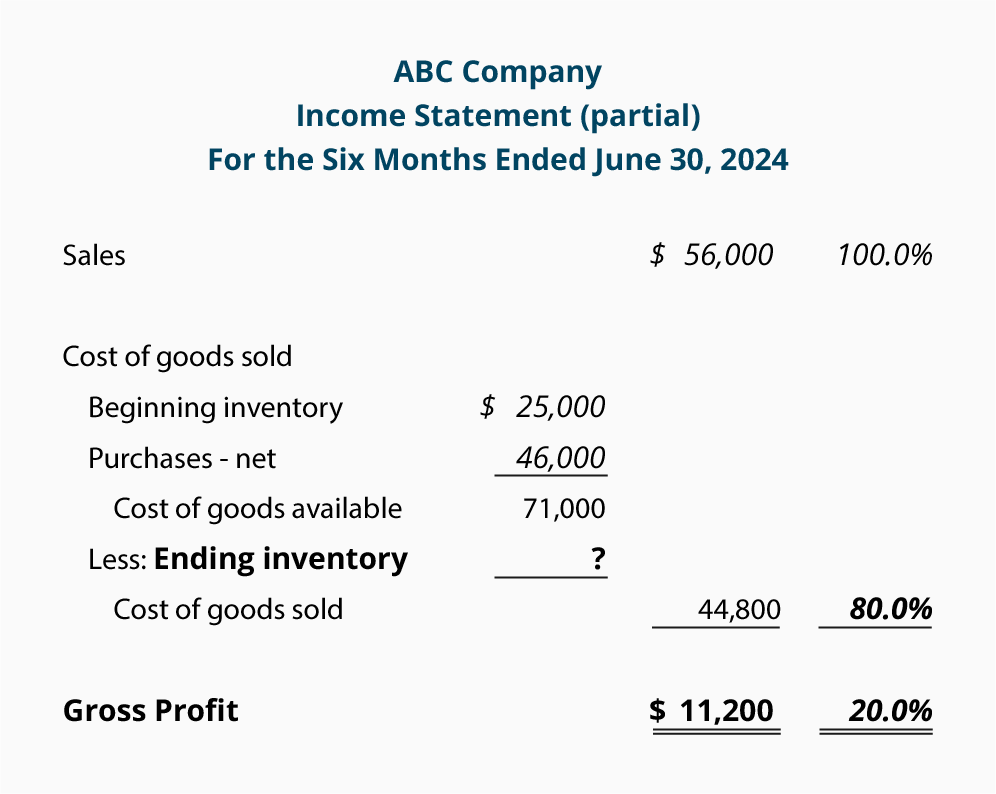

We will fill in the rest of the

statement with the answers to the following calculations. The amounts in italics come from the statement above. The bold amount is the

answer or result of the calculation.

This can also be calculated as 80% x Sales of $56,000

= $44,800.

Inserting this information into the income statement

yields the following:

As you can see, the ending inventory amount is not yet

shown. We compute this amount by subtracting cost of goods sold from the cost

of goods available:

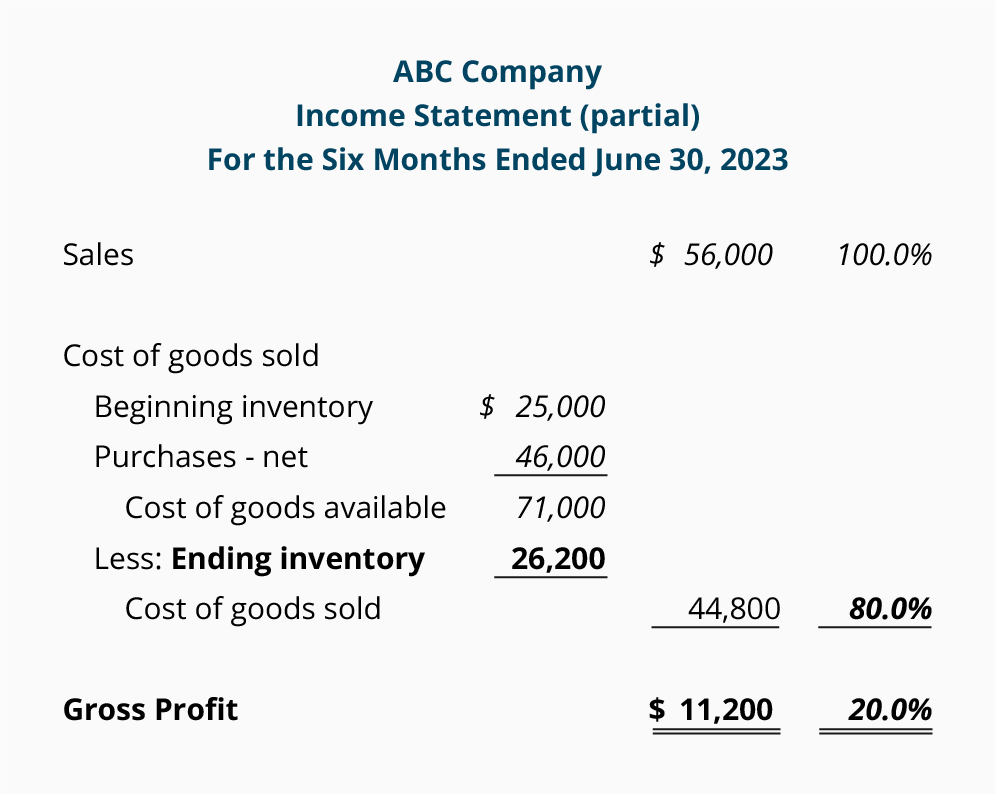

Below is the completed partial income statement with

the estimated amount of ending inventory at $26,200. (Note: It is always a good

idea to recheck the math on the income statement to be certain you computed the

amounts correctly.)

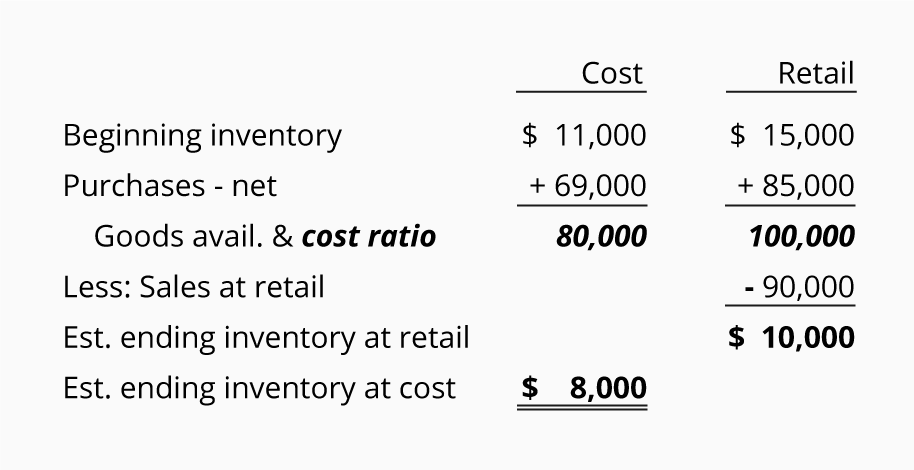

2. Retail Method. The

retail method can be used by retailers who have their merchandise records in

both cost and retail selling prices. A very simple illustration for using the

retail method to estimate inventory is shown here:

As you can see, the cost amounts are arranged into one column. The retail amounts are listed in a separate column. The Goods

Available amounts are used to compute the cost-to-retail ratio. In this case

the cost of goods available of $80,000 is divided by the retail amount of goods

available ($100,000). This results in a cost-to-retail ratio, or cost ratio, of

80%.

To arrive at the estimated ending

inventory at cost, we multiply the estimated ending inventory at retail

($10,000) times the cost ratio of 80%

to arrive at $8,000.

Additional Information and

Resources

Because the material covered here

is considered an introduction to this topic, many complexities have been

omitted. You should always consult with an accounting professional for

assistance with your own specific circumstances.

This comment has been removed by the author.

ReplyDelete